.png)

Unmet financial needs throughout value chains, business ecosystems, and distribution networks is the biggest barrier to growth for corporates. Citibank estimates that approximately 48% of corporates struggle with trapped liquidity where third parties like merchants, distributors, or independents (like volunteers, influencers, or sole traders) lack access to a comprehensive suite of financial products which are relevant to their business. Corporate’s access to a captive distribution network, combined with their understanding of the sector and merchant needs, give them an unfair advantage when it comes to financial services. This enables them to construct a competitive moat around their core offering through increased loyalty and retention, as well as access to new revenue streams.

Co-authored by

Kunal Galav, VP of Product, Toqio

and

Pedro Aires, Director KPMG Spain, KPMG

Despite having access to financial services from traditional banks and neo-fintechs, corporates still haven’t been able to crack the experience. The primary reason is the high degree of standardization of banking products, tech debt for large banks, and limited product offerings by neo-fintechs (due to regulatory timelines).

Traditional banks lack product flexibility

Currently, traditional banks do not have enough flexibility in their product offerings to meet the specific needs of corporate value chains and distribution networks, thus driving a disjointed and limited banking experience.

- There is an arms-length relationship between corporate offerings and bank offerings i.e., separate relationships leading to a lack of competitive advantage, with loyalty to the banking providers rather than the corporate.

- There is a high dependence on bank processes and timelines i.e., lending approval takes over six months, there is a lack of access to PoS solutions, accounts are housed on a single platform.

- There is limited integration between ERP systems and banking providers. Typically, banks lack external APIs which can be connected to modern systems to drive operational efficiencies.

- Neo-fintech providers lack product maturity due to regulatory constraints and burdens. They’re handcuffed to the evolution of the regulatory landscape. For example, they can only offer current accounts without overdraft (which generally doesn’t work for a business).

- Restrictions on product offerings are driven by regulatory timelines rather than technology constraints.

- There is a dependence on provider roadmaps for product customization and integration with business processes, with multi-year lock in contracts.

Four key corporate challenges

Despite leveraging embedded finance and financial services, there is a lack of optionality from traditional banks and neo-fintechs, leading to four key challenges corporates face.

1. Proposition differentiation

Corporates struggle to create unique offerings by leveraging their in-depth knowledge and data on their distribution networks. This limits their ability to tailor products that directly address the specific challenges they face. For example, a large beverage distributor may want better control and visibility over their partner outlets to explore new revenue streams, while a healthcare supplier might be looking for ways to differentiate themselves from competitors to protect their core business. Without the ability to customize offerings, these companies miss out on valuable growth opportunities.

2. Monolithic product offering

Many corporates rely on a single financial services provider, which often results in limited product variety. These companies become locked into the strategies and pricing models of their chosen provider, whether it's a newer Banking-as-a-Service (BaaS) platform or a traditional bank. For instance, a global logistics firm found themselves stuck with high pricing in certain regions just to maintain access to a different market where the provider excels. This lack of flexibility stifles innovation and growth potential.

3. Complex user journeys

The disconnect between corporate business processes and financial products results in fragmented and inefficient customer experiences. This disjointed approach reduces adoption rates and hinders overall growth. Take, for example, non-profit organizations that struggle to automate tasks such as scheduling payments, offering flexible terms, or managing collections. Without seamless integration, these processes remain manual and cumbersome, blocking operational efficiency and financial growth.

4. High implementation costs

Implementing financial services often becomes a costly and lengthy process due to differences in underlying technologies—whether it's outdated legacy systems or newer cloud-native platforms. This complexity drives up integration costs and delays time to market. For instance, major retailers can face operational costs running into tens of millions annually just to maintain their financial services infrastructure, slowing down their ability to innovate and grow.

The evolution of finance and technology: three defining waves

Based on our joint experience throughout Europe and Asia, we see the evolution of embedded finance in three waves:

Winning with financial services in the future

The integration of financial services (FS) into non-financial businesses – is fast becoming a norm internationally, with established players in industries from retail to telecoms. However, despite clearly burgeoning customer demand for ever-greater convenience, adoption of embedded finance remains far from universal.

– KPMG, "Harnessing the power of embedded finance", 2023

In order to capitalize on the third wave and create an unfair advantage within their sectors, corporates need to:

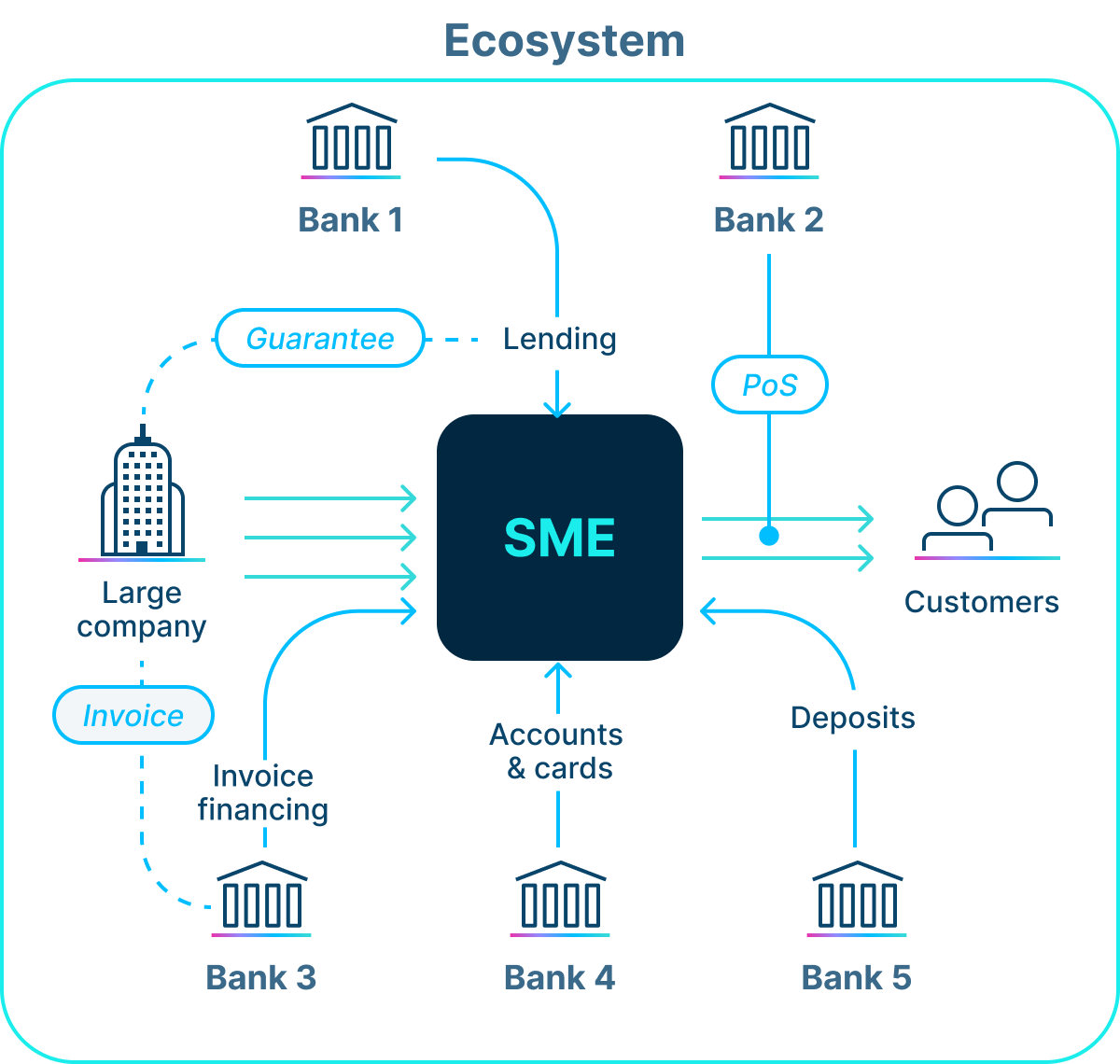

- Orchestrate multiple financial products across various providers (marketplace of providers) which helps bundle the best products from the best providers. For example, a customer in the logistics sector working with Toqio was able to develop a cross-border proposition between Europe and Asia, enabling European webstores to manage their banking products across China, Hong Kong, and 10 European countries. Similarly, a large European brewery working jointly with KPMG and Toqio, integrated accounts and points of sale from various providers, allowing their merchants to streamline revenue collection, ultimately enhancing control and transparency throughout their distribution network.

- Offer customized financial products by configuration to get non-banking tech people to build custom journeys leveraging our low-code platform (based on BPMN and CMMN industry standards). As an example, that same food and beverage customer referenced above, leveraged our low-code platform to build a fully customized onboarding journey with digital signatures in just four weeks, while also offering white-labeled point of sale (PoS) solutions to their merchants at industry-beating rates.

- Integrate complex business logic with financial services, i.e., configure complex payment flows, bridge the gap between ERP and financial services in a contextualized way (rather than a cookie cutter approach). For example, a large global IGO enables automatic fund sweeps for delegates and volunteers in 180 countries, while a global distributor integrated with Shopify and Klarna to manage revenue collection and refunds for their merchants across 10 European countries.

KPMG research predicts the embedded finance industry will reach USD 230 billion in revenue by 2035. We recommend four critical pillars to make it a success:

Technology

|

Partnerships

|

|

|

||

Propositions

|

Efficiency

|

Embracing embedded finance: a strategic path to long-term growth

In conclusion, the future of embedded finance presents immense opportunities for corporates to unlock new revenue streams, enhance customer loyalty, and streamline their financial operations. By leveraging best-in-class financial products, integrating complex business logic, and building customizable, scalable solutions, businesses can create a competitive edge within their sectors. The collaboration between Toqio and KPMG highlights the power of embedded finance to drive operational efficiency and deliver tailored financial services. As we move forward into this next wave of financial evolution, corporates that invest in flexible, innovative solutions will be best positioned to lead the charge, ensuring long-term growth and success.

Meet the authors

|

|

Kunal GalavVice President of Product, ToqioKunal Galav, Toqio’s Vice President of Product, is a massive part of creating innovation in the fintech industry. He has experience in banking and fintech, having worked at HSBC, Mambu, McKinsey and Credit Suisse. Follow Kunal on LinkedIn. |

|

|

Pedro AiresTreasury Director, KPMG SpainPedro Aires has more than 20 years of experience leading IT projects with a clear business orientation. Currently, Pedro is the Treasury project leader at KPMG focused on optimizing treasuries for large corporations. He’s especially adept at the construction and marketing of portfolios of services and products aimed at the financial sector and large corporations. Pedro has extensive experience and knowledge managing internationalization projects for Activities of Consutoria y Telecomunicaciones S.A.where he successfully led on the expansion of its business model in LATAM and PALOP. Follow Pedro on LinkedIn. |